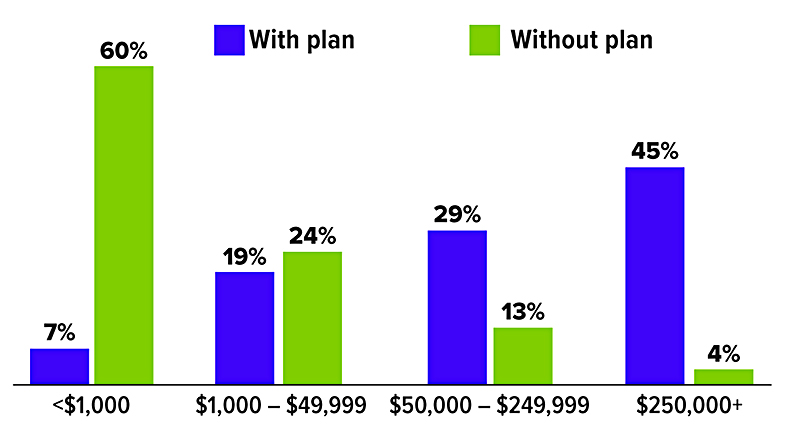

An AARP study released in July 2022 found that nearly half of all private sector employees ages 18 to 64 had no access to a retirement plan at work. It also found that small businesses are more likely to lack a work-based plan, putting their workers at a significant disadvantage when it comes to retirement preparations (see chart).

Last December, Congress passed a $1.7 trillion omnibus package that included the SECURE 2.0 Act of 2022, a sweeping set of provisions designed to improve the nation’s retirement-planning health. Here is a brief look at some of the tax perks, rule changes, and incentives included in the legislation to help small businesses and their employees.1

Tax Perks for Employers in 2023

Perhaps most appealing to small business owners, the Act enhances the tax credits associated with adopting new retirement plans, beginning in 2023.

For employers with 50 employees or less, the pension plan start-up tax credit increases from 50% of qualified start-up costs to 100%. Employers with 51 to 100 employees will still be eligible for the 50% credit. In either case, the credit maximum is $5,000 per year (based on the number of employees) for the first three years the plan is in effect.

In addition, the Act offers a tax credit for employer contributions to employee accounts for the first five tax years of the plan’s existence. The amount of the credit is a maximum of $1,000 per participant, and for each year, a specific percentage applies. In years one and two, employers receive 100% of the credit; in year three, 75%; in year four, 50%; and in year five, 25%. The amount of the credit is reduced for employers with 51 to 100 employees. No credit is allowed for employers with more than 100 workers.

Rule Changes and Relevant Years

In 2024, employers will be able to adopt a starter 401(k) or similar 403(b) plan, an auto-enrollment plan for employee contributions only. The plan may accept up to $6,000 per participant annually ($7,000 for those 50 and older), indexed for inflation. Designed to be lower cost and easier to administer than traditional plans, these programs impose minimum and maximum contribution rates and other rules.

SIMPLE plans may benefit from two new contribution rules. First, employers may make nonelective contributions to employee accounts up to 10% of compensation or $5,000. Second, the annual contribution limits (standard and catch-up) for employers with no more than 25 employees will increase by 10% more than the limit that would otherwise apply. An employer with 26 to 100 employees would be permitted to allow the higher contribution limits if the employer makes either a matching contribution on the first 4% of compensation or a 3% nonelective contribution to all participants, whether or not they contribute. These changes also take effect in 2024.

Beginning in 2025, 401(k) and 403(b) plans will generally be required to automatically enroll eligible employees and automatically increase their contribution rates every year, unless they opt out. Employees will be enrolled at a minimum contribution rate of 3% of income, and rates will increase each year by 1% until they reach at least 10% (but not more than 15%). Not all plans will be subject to this new provision; exceptions include those in existence prior to December 29, 2022, and those sponsored by organizations less than three years old or employing 10 or fewer workers, among others.

Worker Savings Amounts: With Retirement Plan vs. Without

Participant Incentives on the Horizon

SECURE 2.0 drafters were creative in finding ways to encourage workers to take advantage of their plans. For example, effective immediately, employers may choose to offer small-value financial incentives, such as gift cards, for joining a plan, or beginning in 2024, they may provide a matching contribution on employee student loan payments. Also starting in 2024, workers will be able to withdraw up to $1,000 a year in an emergency without having to pay a 10% early distribution penalty, which may ease the fear of locking up savings until retirement (restrictions apply).

1) SECURE stands for Setting Every Community Up for Retirement Enhancement and originated with the SECURE Act of 2019.