Retirees face several unique challenges when managing their income, particularly when it comes to taxes. From understanding how taxes relate to Social Security and Medicare to determining when to tap taxable and tax-advantaged accounts, individuals must juggle a complicated mix of factors.

Social Security and Medicare

People are sometimes surprised to learn that a portion of Social Security income becomes federally taxable when combined income exceeds $25,000 for single taxpayers and $32,000 for married couples filing jointly. The taxable portion is up to 85% of benefits, depending on income and filing status.1

In addition, the amount retirees pay in Medicare premiums each year is based on the modified adjusted gross income (MAGI) from two years earlier. In other words, the cost retirees pay for Medicare in 2023 is based on the MAGI reported on their 2021 returns.

Taxable, Tax-Deferred, or Tax-Free?

Maintaining a mix of taxable, tax-deferred, and tax-free accounts offers flexibility in managing income each year. However, determining when and how to tap each type of account and asset can be tricky. Consider the following points:

Taxable accounts. Income from most dividends and fixed-income investments and gains from the sale of securities held 12 months or less are generally taxed at federal rates as high as 37%. By contrast, qualified dividends and gains from the sale of securities held longer than 12 months are generally taxed at lower capital gains rates, which max out at 20%.

Tax-deferred accounts. Distributions from traditional IRAs, traditional work-sponsored plans, and annuities are also generally subject to federal income tax. On the other hand, company stock held in a qualified work-sponsored plan is typically treated differently. Provided certain rules are followed, a portion of the stock’s value is generally taxed at the capital gains rate, no matter when it’s sold; however, if the stock is rolled into a traditional IRA, it loses this special tax treatment.2

Tax-free accounts. Qualified distributions from Roth accounts and Health Savings Accounts (HSAs) are tax-free and therefore will not affect Social Security taxability and Medicare premiums. Moreover, some types of fixed-income investments offer tax-free income at the federal and/or state levels. 3

The Impact of RMDs

One income-management strategy retirees often follow is to tap taxable accounts in the earlier years of retirement in order to allow the other accounts to continue benefiting from tax-deferred growth. However, traditional IRAs and workplace plans cannot grow indefinitely. Account holders must begin taking minimum distributions after they reach age 73 (for those who reach age 72 after December 31, 2022). Depending on an account’s total value, an RMD could bump an individual or couple into a higher tax bracket. (RMDs are not required from Roth IRAs and, beginning in 2024, work-based plan Roth accounts during the primary account holder’s lifetime.)

Don’t Forget State Taxes

State taxes are also a factor. Currently, seven states impose no income taxes, while New Hampshire taxes dividend and interest income and Washington taxes the capital gains of high earners. Twelve states tax at least a portion of a retiree’s Social Security benefits.

Eye on Washington

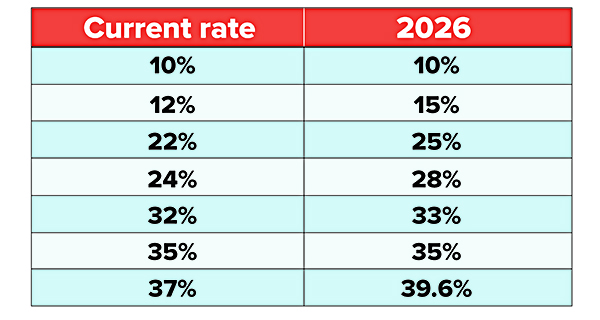

Finally, both current and future retirees will want to monitor congressional actions over the next few years. That’s because today’s historically low marginal tax rates are scheduled to revert to higher levels in 2026, unless legislation is enacted (see table).

Help Is Available

Putting together a retirement-income strategy that strives to manage taxes is a complex task indeed. Investors may want to seek the help of a qualified tax or financial professional before making any final decisions.4

Tax Rates Scheduled to Rise

Unless legislation is enacted, federal marginal income tax rates are scheduled to rise in 2026.

1) Combined income is the sum of adjusted gross income, tax-exempt interest, and 50% of any Social Security benefits received.

2) Distributions from tax-deferred accounts and annuities prior to age 59½ are subject to a 10% penalty, unless an exception applies.

3) A qualified distribution from a Roth account is one that is made after the account has been held for at least five years and the account holder reaches age 59½, dies, or becomes disabled. A distribution from an HSA is qualified provided it is used to pay for covered medical expenses (see IRS publication 502). Nonqualified distributions will be subject to regular income taxes and penalties.

4) There is no guarantee that working with a financial professional will improve investment results.

The articles and opinions expressed in this document were gathered from a variety of sources, but are reviewed by Strickland Financial Group, LLC prior to its dissemination. Any articles written by Graham M. Strickland or Strickland Financial Group will include a ‘by line’ indicating the author. Strickland Financial Group provides a full range of financial services, including but not limited to: life, health, disability and long term care insurance, group and individual retirement plans and individual investments. Receipt of literature in no way implies suitability of product(s) in your financial plan. Strickland Financial Group maintains networking relationships with estate planning attorneys and tax professionals but does not itself offer legal or tax advice. Securities offered through Triad Advisors, LLC (TRIAD), Member FINRA/SIPC. Advisory services offered through S&S Wealth Management, LP (S&S). A Registered Investment Advisor. Strickland Financial Group is independent of TRIAD and S&S.

This communication is strictly intended for individuals residing in the state(s) of NE and TX. No offers may be made or accepted from any resident outside the specific states referenced.

Prepared by Broadridge Advisor Solutions Copyright 2023.